Expenditure Or Revenue?

Recall my earlier information – that the 2011 loss under the ‘restatement’ only increased by the $3.1 million broadcast revenue recalculation so the key question then becomes how is it possible that the overall expenditure number has increased by $9.877 million yet there is no corresponding increase in the 2011 loss?

Recall my earlier information – that the 2011 loss under the ‘restatement’ only increased by the $3.1 million broadcast revenue recalculation so the key question then becomes how is it possible that the overall expenditure number has increased by $9.877 million yet there is no corresponding increase in the 2011 loss?

The answer is very curious – 2011 reported revenue has been increased under the ‘restatement’ with that increase matching the increase in expenditure (after deducting the $3.1 million referred to earlier)!

How do you increase reported revenue to cover an increase in reported expenditure? The answer, or rather a clue, can be found in one sentence on page 95 of the 2012 annual report.

Presentation of revenue comparatives in the Income Statement have been changed from a net to gross basis

In the summary in the annual report titled “How The Numbers Stack Up” there is one additional comment.

The Income Statement now provides analysis of revenue on a gross basis, and analysis of expenditure on a functional basis. This format provides more meaningful analysis of the operations of the business.

That’s it – there is no more explanation provided by the ARU and specifically no comment on the changes to the expenditure comparatives.

It falls to Green and Gold Rugby to explain what has happened here and I’m thankful for the input from a number of our members who are accountants for their input and review of the accounting issues.

Whilst the world of accounting can be very confusing with many different standards and policies dictating how financial statements should be prepared, how profit is calculated and how assets and liabilities should be measured; the basic concept for determining the profit or loss of a business is:

Revenue (or Sales) less Direct Costs =Gross Profit less Overheads = Net Profit

As an example, in the ARU’s case if the ticket sales from a test match were $5 million and the costs related to that match including player match payments were $3 million, the gross profit for the ARU from that match would be $2 million. From the gross profit for all matches and adding in other revenue (such as broadcast revenue and sponsorship) the ARU would deduct overheads to arrive at a net profit figure for the year.

In 2011 the ARU’s accounting policy was that rather than reporting gross revenue and the related expenditure separately a ‘net’ revenue figure was reported. Using the previous example of a test match this would mean disclosing revenue of only $2 million without disclosing the deduction of expenditure from the revenue to arrive at that ‘net’ revenue amount. The amount of expenditure related to that revenue was not disclosed in the financial statements and nor was the full revenue.

Imagine in your own business if you sold an item for $1,000 that you had bought for $600 – would you report sales of $400 and no expenditure in relation to that sale? I doubt it but that’s exactly what the ARU did in 2011.

There was no disclosure in the original 2011 annual report that this ‘net’ method of recording revenue and expenditure was being used. There is no mention of this policy on pages 94-99 of the annual report which is headed ‘Significant Accounting Policies’ – maybe this policy wasn’t deemed significant enough to include! There is a clue in the name of one of the revenue categories – ‘Net Gate Takings’. That discloses a lot – surely we all should have understood what was going on from that description!

The Australian Accounting Standard AASB118 includes a definition of revenue – “Revenue is the gross inflow of economic benefits during the period …”. With the accounting standard requiring the measurement of revenue on a gross basis, why did the ARU disclose revenue on a net basis? That’s a question only the ARU or their auditors can answer.

Under the ‘restatement’ I’d expect to find items of reported expenditure like ticket commissions, match day costs and maybe match payments for players to increase as part of the ‘restatement’ because they would be the sorts of expenditure you would expect to be considered direct costs of revenue and therefore previously ‘netted’ off against revenue.

Look at the table I included earlier and you can see that there was very little reported increase in these sorts of expenditures. There are two new categories under the ‘restatement’ – commissions and marketing. If you were going to ‘net’ off expenditure directly related to revenue those are the sorts of expenditure you’d expect would have been used. However, there is only one reported expenditure item that has increased significantly under the ‘restatement’ – the $7.1 million increase in ‘Corporate’ expenditure.

The ‘restatement’ of the 2011 results shows that at least in that year the ARU deducted $7.096 million of ‘Corporate’ expenditure plus a further $0.536 million, being its share of the SANZAR office costs, from revenue – that’s 50% of its overheads not disclosed as expenditure at all by ‘netting’ it off against revenue rather than reporting it in the expenditure section of the financial statements.

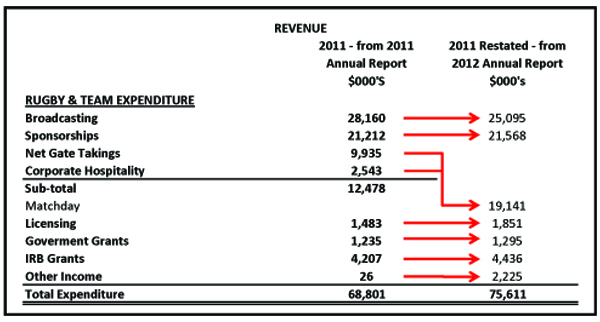

Here are the ‘restated’ revenue numbers for 2011.

As you can see the biggest area of increase is in the category now called ‘Matchday’ which is $6.663 million higher under the ‘restatement’. There is also an increase of around $2 million in ‘Other Income’. It therefore appears that the majority of ‘Corporate’ expenditure not previously reported was deducted from the previous categories of ‘Net Gate Takings’ and ‘Corporate Hospitality’. The use of the word ‘net’ in the gate takings category also gives us another clue as to where the “Corporate’ expenditure may previously have been ‘netted’ off against.